Haven

Unlocking the Value of Affordable Homeownership

Private Fundraise

This company may be interested in raising funds from accredited investors. You must Request Access to see more information about this company.

Request Access 9

INTRODUCING HAVEN

You’re home — for less.

Haven fractionalizes housing.

Haven facilitates capital.

Haven fuels homeownership.

And makes it affordable — and financially sound.

Haven facilitates real estate investing alongside the down payments of creditworthy homebuyers.

Investors invest capital: on a passive, efficient, and diversified basis. And gain access to levered, double-digit returns.

Renters, for the first time in a generation, turn into homeowners, qualifying for a mortgage while borrowing less — and at a lower interest rate while eliminating PMI (Private Mortgage Insurance).

Haven invigorates the Pursuit of the American Dream.

HAVEN: FAST FACTS

HURDLES TO THE AMERICAN DREAM

There's a distinct gap in the accessibility of homeownership and the pursuit of the American Dream.

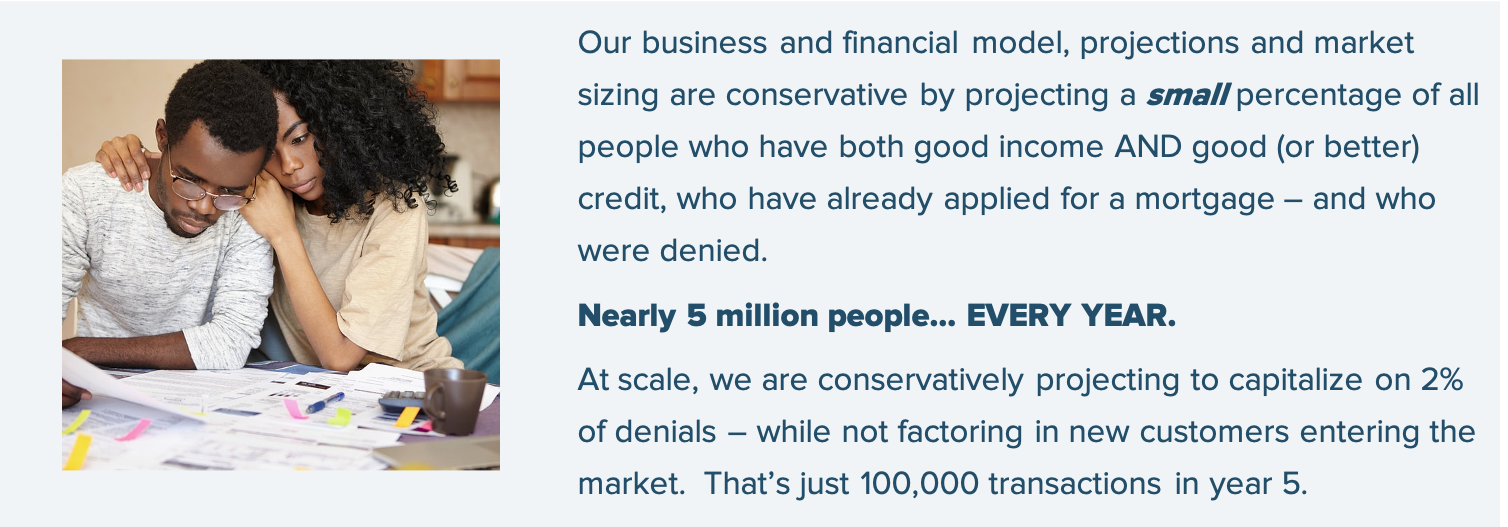

There are more than $450 billion in mortgages denied every year to people with good income (over $100K annually) and good (very good, or excellent) credit. (Nearly $600 billion in total mortgages denied, inclusive of those with fair/poor credit, or less than good income.)

There are more than $450 billion in mortgages denied every year to people with good income (over $100K annually) and good (very good, or excellent) credit. (Nearly $600 billion in total mortgages denied, inclusive of those with fair/poor credit, or less than good income.)

All too often this is due to: (1) Insufficient money for a down payment to qualify for a mortgage, or to make monthly payments affordable, or (2) Debt-to-Income Ratio being just slightly too high.

It's time to change that.

ONE REVOLUTIONARY SOLUTION

Haven provides investors with a solution to both passively and efficiently invest in:

Haven allows investors to co-invest up to an equal amount of capital alongside homebuyers’ down payments, acting as de facto (silent) partners on properties.

Investors deploy their co-investment capital towards a cumulative down payment, without having to pay:

We allow investors the benefits of levered returns – they see returns on much more of the property than they are financing, as the homebuyers/homeowners pay the costs of that leverage (homeowners are responsible for the loan).

With Haven, investors can avoid these common issues:

- Unaligned tenants that may cause damage during renting

- The likelihood of vacancies and managing turnover

- Selling properties at a discount while tenants are still occupying

- Forcing early vacancies in order to sell their properties

Haven allows investors to decide the terms on which to deploy their capital. In our consumer-friendly approach, we provide homebuyers with offers on a deal-by-deal basis, curating the best terms sourced through our marketplace.

Haven allows investors to decide the terms on which to deploy their capital. In our consumer-friendly approach, we provide homebuyers with offers on a deal-by-deal basis, curating the best terms sourced through our marketplace.

Competition amongst investors creates attractive, market-driven offers to homebuyers, fueling demand for co-investment capital. Over time, this generates more investor appetite for the asset class, resulting in more volume in owner-occupied housing. Then, through our exchange platform, we’re able to deliver on our ultimate objective: creating liquidity for real estate investors.

WE HELP MILLENNIALS AFFORD

THEIR FIRST HOME

Many real estate verticals have written off Millennials (ages 23-38) as homeowners.

Many real estate verticals have written off Millennials (ages 23-38) as homeowners.

And they are wrong to do so.

We firmly believe -- and the data shows -- that more than ever Millennials are seeking to enter the housing market.

They identify barriers to entry and obstacles that can be easily overcome given a new solution. For example, in a recent study, Freddie Mac (April 2019 – The Harris Poll Consumer Omnibus Results) found that between 46% and 50% of Millennials who are currently renters said they desire and expect to become homeowners.

This is at an all-time high, up from the low-to-mid 20 percentile range just a few years ago.

Of those identified as prospective homebuyers, 47% stated they hope to do so in the next two years.

This equates to tens of millions of potential new customers entering the housing market.

REMOVING BARRIERS

The aforementioned study found that these renters identify large barriers to entry, including these top two:

Overall the data shows both in attitude and in concrete action, Millennials are planning to enter the housing market and see the benefits of doing so.

We firmly believe a creative and innovative solution that both bridges the down payment gap and lowers borrowers’ monthly payments could finally make homeownership possible for millions of Americans.

THIS ISN’T SPECULATIVE

We aren’t talking about changing behaviors.

We aren’t talking about hopeful new entrants into the market.

We could have 10 other companies enter the market and replicate exactly what we are doing at scale – and we’d still see that as a boon to our business, as it would make equity co-investments more popular and bring greater awareness to this type of innovative financing.

In other words, Haven isn’t wishful thinking. It’s very plausible.

BUILT FOR INVESTORS, TOO

This is bigger than Millennials alone.

This is bigger than Millennials alone.

The investor market is underserved when it comes to residential real estate. Currently, there is no way for third-party investors to both passively and efficiently invest in residential real estate – and on a diversified basis.

Yet, there’s the demand for it:

One-third of homes in the United States are owned by investors.

But those investments have generally been relegated to REITs (which tend to skew commercial, and the returns for which are reduced when interest rates or vacancies rise). Those investments have also been relegated to properties in investors’ local markets, as they are high-touch due to management requirements associated with rental properties.

Haven will change all of that – PASSIVE, EFFICIENT, DIVERSIFIED INVESTING.

HOW IT WORKS – AND THRIVES

At a minimum, homebuyers must put down 10% of the value of their home. At a maximum, investors can agree to match that down payment, meaning homebuyers must have equal to, or more, skin in the game as their co-investor(s).

We require a minimum of 20% down combined from both parties to eliminate PMI, resulting in even greater payment savings to the homebuyer / homeowner. By doing so, our guidelines make Haven a better, more affordable solution for homebuyers versus buying homes on their own (not to mention significantly better compared to renting).

We require a minimum of 20% down combined from both parties to eliminate PMI, resulting in even greater payment savings to the homebuyer / homeowner. By doing so, our guidelines make Haven a better, more affordable solution for homebuyers versus buying homes on their own (not to mention significantly better compared to renting).

Haven was designed to produce better, more competitive returns for investors than alternative investment vehicles for deploying capital into the housing market today.

FINANCING SCENARIOS

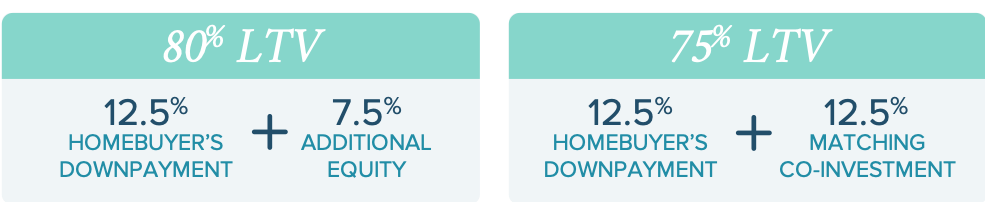

As an example, a homebuyer places 12.5% of their home value in the form of a down payment. The homebuyer could seek to source a minimum of 7.5% in additional equity through our platform for an 80% LTV (Loan-to-Value). They could also request as much as 12.5% (a matching co-investment) in equity, which would result in a 75% LTV.

The standard use case for a homebuyer coming to Haven, would be to put down 10% and seek a matching co-investment of 10% through our platform, resulting in an 80% LTV.

The standard use case for a homebuyer coming to Haven, would be to put down 10% and seek a matching co-investment of 10% through our platform, resulting in an 80% LTV.

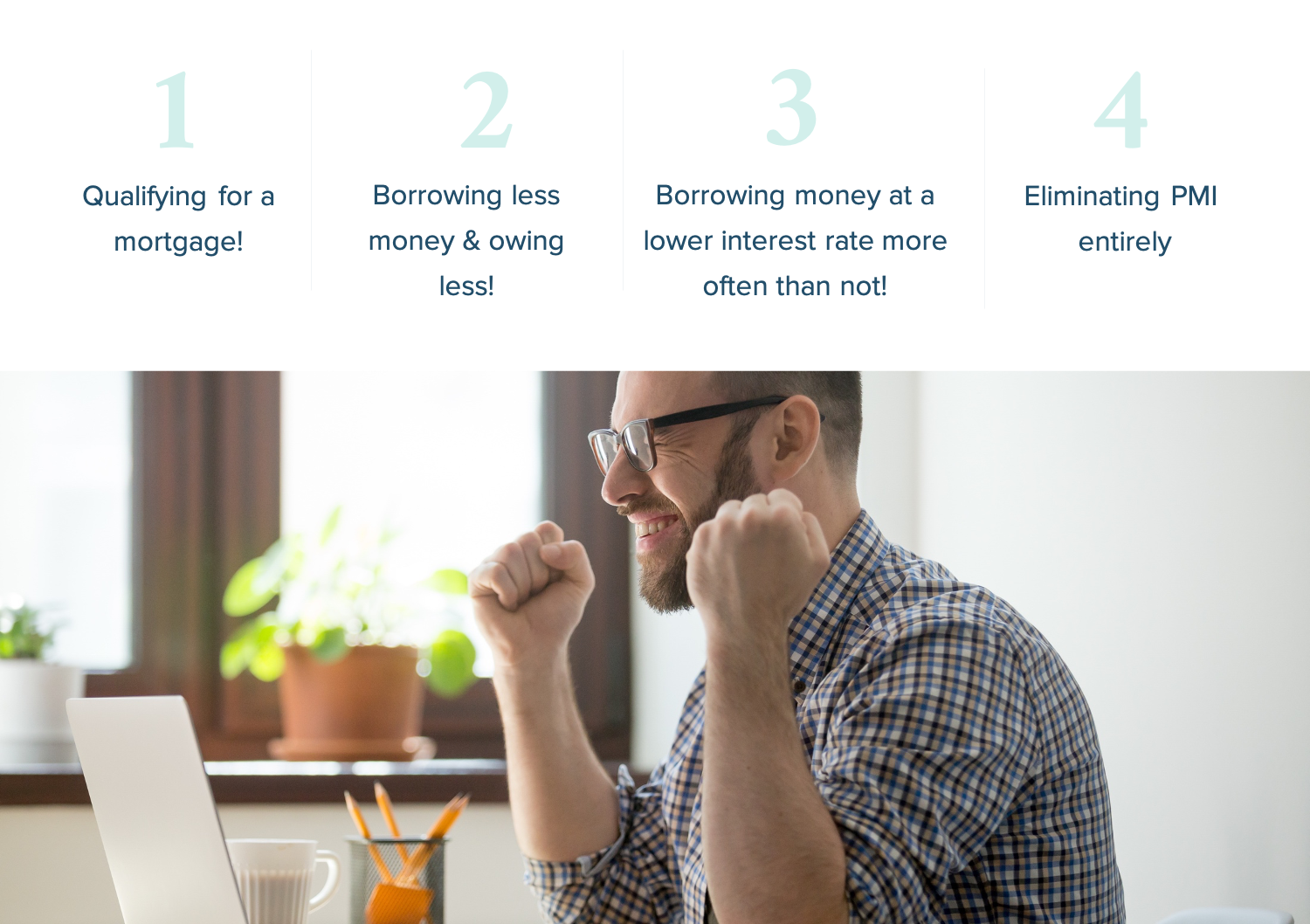

More money down – cumulatively between the homebuyer’s down payment and the investor’s co-investment – typically results in four things:

GO-TO-MARKET

We will generate investor appetite and interest in our first Crowdfund Sidecar Fund (a target $10M raise with target minimum $50,000 investments per person) through our investor-oriented content strategy.

We will generate investor appetite and interest in our first Crowdfund Sidecar Fund (a target $10M raise with target minimum $50,000 investments per person) through our investor-oriented content strategy.

We will fund the equity co-investments of our next ~150 deals from this Crowdfund Sidecar Fund. In this phase, we will act as the investor, deploying capital on behalf of a subset of investors.

Concurrently, we will focus on raising our Main Sidecar Fund (target $50M), which is capable of funding our next ~750 deals. One of our co-founders is solely focused on the raise and we have a commitment from the European Family Office already invested in Haven. We will deploy investors’ capital on their behalf into the transaction, based on a series of guidelines and benchmarks. The goal is to ensure that any interaction with Haven results in no slowdown to the home-buying process in our first year of operation.

Concurrently, we will focus on raising our Main Sidecar Fund (target $50M), which is capable of funding our next ~750 deals. One of our co-founders is solely focused on the raise and we have a commitment from the European Family Office already invested in Haven. We will deploy investors’ capital on their behalf into the transaction, based on a series of guidelines and benchmarks. The goal is to ensure that any interaction with Haven results in no slowdown to the home-buying process in our first year of operation.

ADDRESSING COVID-19 &

RECESSION CONCERNS

We're not saying this to make light of the current pandemic, but we want to convey that Haven is a strong tech start-up investment opportunity – and we aren’t projecting for a growth phase until well into 2021.

Through Fall 2020, our plans only call for 5 transactions – and by end of year, another 50. Through Summer 2021, we hope to get to a cumulative total of 750 transactions. And only after then do we intend to really scale the business.

Why is Haven not just recession-proof, but likely to be successful nonetheless during difficult economic times?

Investors want to put their capital into a more secure asset class, in light of what is happening in the public markets.

Investors want to put their capital into a more secure asset class, in light of what is happening in the public markets.

Homebuyers/Consumers want to keep more of any capital that they have saved in a bank account ”for a rainy day” and are more likely to entertain a co-investor in their property.

Homebuyers/Consumers want to keep more of any capital that they have saved in a bank account ”for a rainy day” and are more likely to entertain a co-investor in their property.

Banks & Lenders will look to generate as much business as possible to make up for a possible slowdown, thereby more likely to entertain innovative partnerships such a Haven and the financing structures we bring.

Banks & Lenders will look to generate as much business as possible to make up for a possible slowdown, thereby more likely to entertain innovative partnerships such a Haven and the financing structures we bring.

Even if or as the economy dips, it won’t impact our ability to grow our business. This is based not on conjecture, but on hard evidence that comes from the roughly 4.7 million mortgage denials every year.

Even if or as the economy dips, it won’t impact our ability to grow our business. This is based not on conjecture, but on hard evidence that comes from the roughly 4.7 million mortgage denials every year.

There's a large market for what we offer, so our product is obviously needed.

DOES THIS RECESSION HAVE AN IMPACT?

Unlike the Great Recession, this Recession wasn’t caused by the real estate market. The last recession was largely fueled by the foreclosure crisis and the downturn in the housing market.

A report by First American Financial Services suggests that the housing market may actually aid the economy in recovering from the next recession — a role it has traditionally played in previous economic recoveries. With the exception of the Great Recession, house price appreciation hardly skipped a beat and year-over-year existing-home sales growth barely declined in all the other previous recessions in the last 40 years.

A report by First American Financial Services suggests that the housing market may actually aid the economy in recovering from the next recession — a role it has traditionally played in previous economic recoveries. With the exception of the Great Recession, house price appreciation hardly skipped a beat and year-over-year existing-home sales growth barely declined in all the other previous recessions in the last 40 years.

Overall, homeowners have very high levels of available home equity today, providing a cushion to withstand potential price declines.

Unlike previous recessions, this recession starts with a housing shortage – a supply shortage. A recession is likely to worsen the conditions causing the housing shortage, potentially making housing costs even less affordable for buyers and renters. Less affordable means Haven is further necessary.

Returns for real estate investors will be stronger in certain up-and-coming cities and suburbs than in primary markets, and Haven is poised to capitalize on that.

Returns for real estate investors will be stronger in certain up-and-coming cities and suburbs than in primary markets, and Haven is poised to capitalize on that.

What made the Great Recession different? The housing boom that preceded the last recession was largely driven by an explosion in both home-building activity and mortgage credit. Homebuyers were able to get mortgages with no documentation of their income and no down payment, and many loans had introductory 0% interest periods that made them cheap to start but more expensive as time wore on. These homeowners were over-leveraged.

MEET THE TEAM

Khalid Itum

Khalid Itum

Founder and CEO

- Former EVP of MoviePass (October 2018 through March 2019)

- Former Vice President of Business Development & Studio Relations of MoviePass

- Investor & Advisor

- Serial Entrepreneur: Commercial Real Estate, Banking, Tech, International Travel

Jake Petersen

Jake Petersen

Co-Founder, Operations

- Khalid recruited him to MoviePass and when Khalid was promoted to run the day-to-day business there, and Jake served as his right hand, overseeing all operations on Khalid’s management team

- 8+ years of Customer Experience working with some of the fastest growing companies in tech, including Apple, Tinder, Oscar Health, Houzz, and Shopify

Gregory Jacobson

Gregory Jacobson

Co-Founder, Capital Formation

- Oversees capital formation activities as they relate to the investor community and its sidecar funding strategy

- Dealmaker and investor and represents private family office capital out of Europe and the United Kingdom

Zac Bright

Zac Bright

Co-Founder, Special Projects

- Primarily responsible for pushing forward key, high-priority initiatives and special projects initiated by Haven's CEO

- Secondarily responsible for bringing high-value relationships into the Haven fold both externally and internally

Julie Suh

Julie Suh

Data + Analytics Lead

- Advises on Data Strategy

- Developing consumer-friendly Rent versus Own and Own Alone versus Own with Haven models

- Financial Accounting + Data Analytics Professor – University of Southern California

- Financial Accounting Professor, Outstanding New Instructor Award – University of California – Berkeley

- Investment Banking Analyst – Goldman Sachs Stanford University, Ph.D. Business Administration Wellesley College, BA, Economics

Luke Peterson

Luke Peterson

Lender Partnerships + Business Development

- Extensive banking and lending experience, having previously served as President of U.S. Operations at Geenee, as well as Managing Director of First Republic Bank, Director of Acquisitions at Republic Investment Company, and as a Private Mortgage Banker at Wells Fargo

The Advisory Board

Jere Simpson

Jere Simpson

- Founder & CEO, Kitewire

- Founder, dot.com

- Former Advisor, Executive Office of Presidents Bush & Obama

Dario Meli

Dario Meli

- Co-Founder, Hootsuite

- Founder & Chairman, Quietly

Ryan Withall

Ryan Withall

- Director of Acquisitions and Development, Lincoln Avenue Capital

James Healy

James Healy

- Adjunct Professor of Fintech, University of Southern California

- Former CFO of Icahn Automotive Group

- Previously VP of Business Development at FastPay, Fintech lending & payments company

- Various Leadership Roles, GE Capital

Rudy Baldoni

Rudy Baldoni

- CEO, Newport Investment Associates

Rodes Ponzer

Rodes Ponzer

- Founder, Rodes Advisory

- Former Global Brand Leader, TBWA\Chiat\Day

- Former Executive Vice President & Management Director, Saatchi & Saatchi

TRACTION & ACCOMPLISHMENTS

After months of focused effort, Haven is proud to have developed the legal structure for the home purchase transaction in the form of a trust agreement, based on numerous iterations informed by lender feedback, and rigorous and entrepreneurial know-how from our partner law firms.

We have also tested this agreement with lenders by iterating on a Term Sheet, ensuring that the structure is acceptable to mortgage lenders originating mortgages for our customers, alongside our equity capital investments.

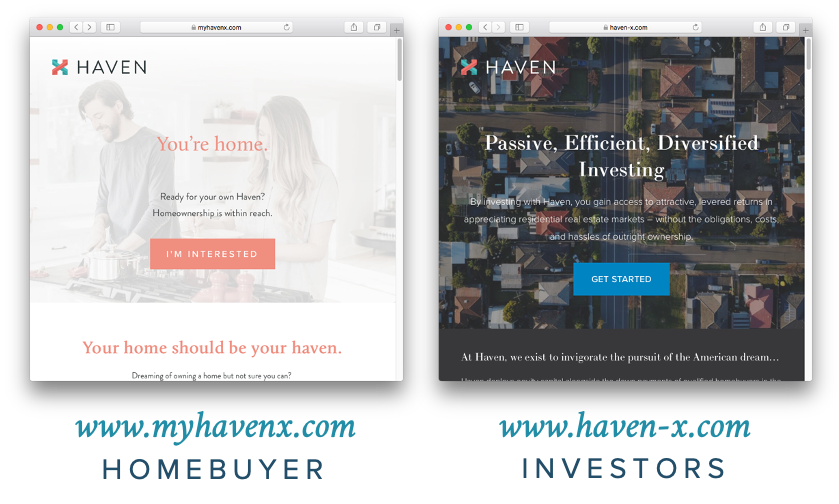

We launched public-facing marketing sites for both homebuyer (www.myhavenx.com) and investor (www.haven-x.com) and with zero marketing spend and just a handful of posts to Facebook & Instagram (for homebuyers) and social shares on LinkedIn (for investors), we have generated a great deal of interest and inbound inquiries from both homebuyers and investors.

We launched public-facing marketing sites for both homebuyer (www.myhavenx.com) and investor (www.haven-x.com) and with zero marketing spend and just a handful of posts to Facebook & Instagram (for homebuyers) and social shares on LinkedIn (for investors), we have generated a great deal of interest and inbound inquiries from both homebuyers and investors.

Investor expressions of interest showed a range of $50,000 to $1M in annual investments in residential real estate.

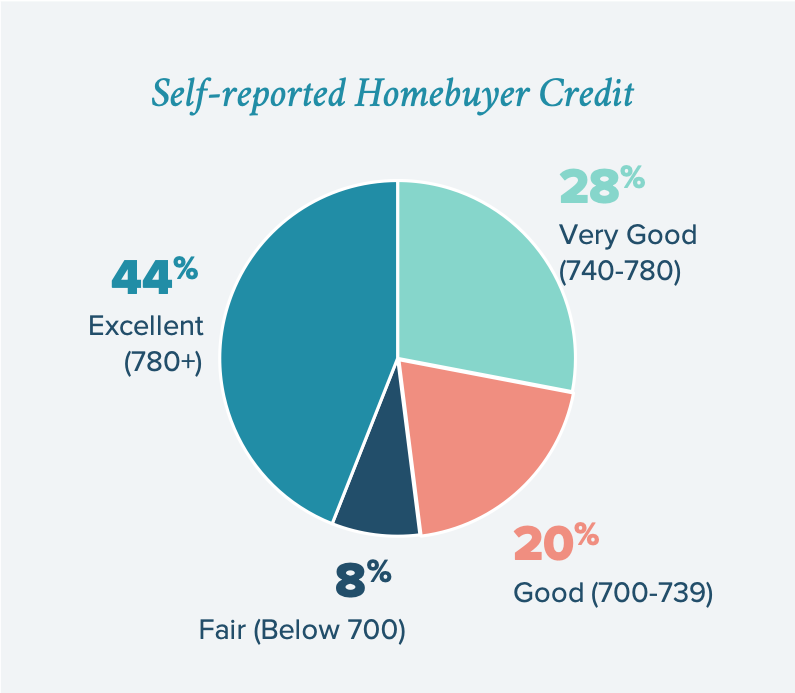

Self-reported Homebuyer Credit came in at: 44% Excellent (780+), 28% Very Good (740-780), 8% Fair (Below 700), 20% Good (700-739). Removing only a couple of outlier data points, Median Self-Reported Annual Income was at $185,000, Lowest Self-Reported Annual Income was at $100,000, and Highest Self-Reported Annual Income reported was at $510,000. Average monthly rent payment is $2,700; most are current renters versus existing homeowners; and interest has been expressed primarily from Los Angeles, Southern California, Seattle, the Bay Area, Chicago, New York, and even… London (but our plans are currently Domestic in scope).

Self-reported Homebuyer Credit came in at: 44% Excellent (780+), 28% Very Good (740-780), 8% Fair (Below 700), 20% Good (700-739). Removing only a couple of outlier data points, Median Self-Reported Annual Income was at $185,000, Lowest Self-Reported Annual Income was at $100,000, and Highest Self-Reported Annual Income reported was at $510,000. Average monthly rent payment is $2,700; most are current renters versus existing homeowners; and interest has been expressed primarily from Los Angeles, Southern California, Seattle, the Bay Area, Chicago, New York, and even… London (but our plans are currently Domestic in scope).

We aim to close our first transaction by September 1, 2020.

-

INTRODUCING HAVEN

-

HAVEN: FAST FACTS

-

HURDLES TO THE AMERICAN D...

-

ONE REVOLUTIONARY SOLUTIO...

-

WE HELP MILLENNIALS AFFOR...

-

REMOVING BARRIERS

-

THIS ISN’T SPECULATIVE

-

BUILT FOR INVESTORS, TOO

-

HOW IT WORKS – AND THRIVE...

-

FINANCING SCENARIOS

-

GO-TO-MARKET

-

ADDRESSING COVID-19 & REC...

-

DOES THIS RECESSION HAVE...

-

MEET THE TEAM

-

THE ADVISORY BOARD

-

TRACTION & ACCOMPLISHMENT...